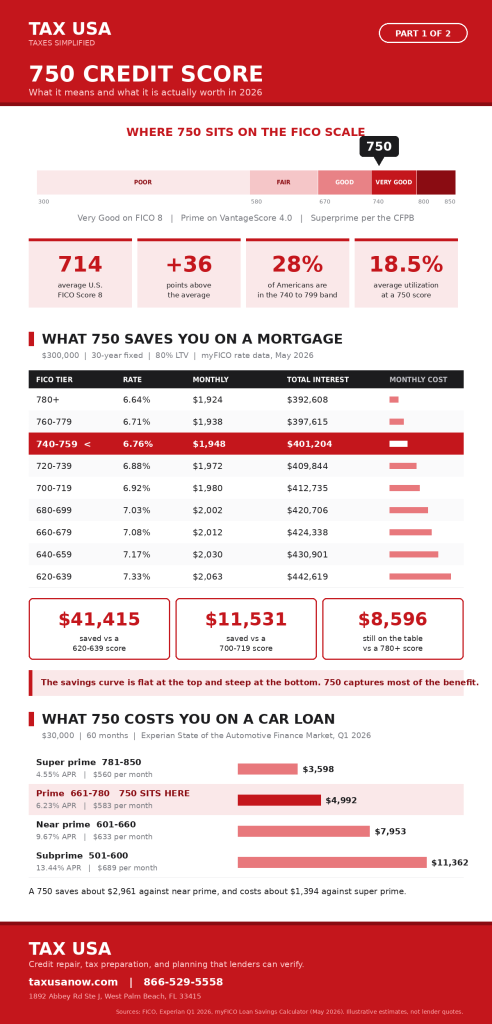

A 750 credit score places you in the Very Good tier of the FICO Score range and in the super prime tier that most lenders price their best offers around. It is not a perfect number, but it is the number at which borrowing gets meaningfully cheaper. On the FICO Score 8 scale of 300 to 850, a 750 credit score sits inside the 740 to 799 band, comfortably above the national average and close enough to the Exceptional range that the remaining gap is worth understanding.

The practical question is not whether 750 is good. It is what 750 actually buys you in 2026 pricing and what separates it from 800. This guide answers both questions using current lender data from FICO, Experian, and the myFICO Loan Savings Calculator, then shows the specific credit behaviors that move a score in either direction. Tax USA works with clients on exactly this problem through our credit repair services, so the guidance below reflects what lenders reward in practice, not theory.

Where a 750 Credit Score Falls in the Credit Score Ranges

Credit scores are grouped into tiers. Each tier maps to a different risk assumption and a different price.

| FICO Score 8 Range | Rating | Share of U.S. Consumers | What Lenders Assume |

|---|---|---|---|

| 300 to 579 | Poor | 13% | High default risk; secured products only |

| 580 to 669 | Fair | 16% | Subprime pricing: approval is conditional |

| 670 to 739 | Good | 21% | Average risk; standard rates |

| 740 to 799 | Very Good | 28% | Low risk; competitive rates and premium products |

| 800 to 850 | Exceptional | 22% | Lowest risk; best available terms |

Source: Experian, FICO Score 8 distribution.

A 750 credit score sits in the fourth band. Roughly half of American consumers score below the Very Good threshold, which is why this number carries real weight at underwriting.

FICO Score vs VantageScore treatment of 750

The two dominant scoring models label 750 differently, and this trips up a lot of borrowers.

- FICO Score 8: 750 is Very Good. The Exceptional tier starts at 800.

- VantageScore 4.0: 750 is Prime. The Super Prime tier starts at 781.

- Consumer Financial Protection Bureau: any score above 720 is classified as superprime, the agency’s highest profile.

So the same score can be called Very Good, Prime, or superprime depending on who is describing it. What matters is the tier your specific lender prices from, and most mortgage lenders price in 20-point increments regardless of the label.

How 750 compares to the national average

The average FICO Score 8 in the United States was 714 as of early 2026. The average VantageScore 3.0 was closer to 698. A 750 credit score is roughly 36 points above the FICO average.

For auto lending, the comparison is tighter. The average VantageScore for new auto loan applicants was 751 in the first quarter of 2026, according to Experian’s State of the Automotive Finance Market report. For used auto loans, the average applicant scored 682. A 750 credit score is average for a new car buyer and well above average for a used car buyer.

What a 750 Credit Score Tells Lenders

Lenders do not read your score as a character judgment. They read it as a default probability. This is risk-based pricing, and it is standard across U.S. consumer lending.

The risk profile behind the number

Experian’s data on consumers scoring 750 shows a consistent behavioral pattern:

- About 1% of consumers in the Very Good range become seriously delinquent in the following period.

- Late payments appear on roughly 24% of credit reports belonging to 750 scorers.

- The average credit utilization rate among 750 scorers is 18.5%.

- Around 36% carry an auto loan, and 33% carry a mortgage.

That last set of figures is the most useful. It tells you a 750 credit score is usually built on a mixed file with installment debt, not on credit cards alone.

Approval odds and what the score does not cover

A 750 credit score strongly improves approval odds, but it does not approve you by itself. Underwriters also weigh:

- Debt-to-income ratio. A 750 score with a 50% DTI still gets declined for a mortgage.

- Length of credit history. A 750 built over 18 months reads differently than one built over 15 years.

- Loan-to-value ratio. Mortgage rate tables assume 80% LTV. A smaller down payment changes your rate regardless of score.

- Employment and income stability. Documented, consistent income supports the file.

- Score version used. Lenders may pull FICO 2, 4, 5, 8, 9, 10 T, or an industry-specific auto or bankcard score. Your number can shift by 20 points or more between versions.

Two borrowers with identical 750 scores can receive different offers from the same lender for these reasons.

What a 750 Credit Score Saves You in 2026

This is where the number stops being abstract.

Mortgage rates at a 750 credit score

The table below reflects the myFICO Loan Savings Calculator on a $300,000, 30-year fixed mortgage at 80% LTV, using May 2026 rate data sourced from Curinos LLC. A 750 credit score falls in the 740 to 759 tier.

| FICO Score Tier | Estimated Rate | Monthly Payment | Total Interest (30 years) |

|---|---|---|---|

| 780 and above | 6.64% | $1,924 | $392,608 |

| 760 to 779 | 6.71% | $1,938 | $397,615 |

| 740 to 759 (750 sits here) | 6.76% | $1,948 | $401,204 |

| 720 to 739 | 6.88% | $1,972 | $409,844 |

| 700 to 719 | 6.92% | $1,980 | $412,735 |

| 680 to 699 | 7.03% | $2,002 | $420,706 |

| 660 to 679 | 7.08% | $2,012 | $424,338 |

| 640 to 659 | 7.17% | $2,030 | $430,901 |

| 620 to 639 | 7.33% | $2,063 | $442,619 |

Figures are illustrative estimates, not lender quotes.

Three conclusions follow from this table:

- Against a 620 to 639 score, a 750 saves $115 per month and $41,415 in interest over the life of the loan.

- Against a 700 to 719 score, a 750 saves $32 per month and $11,531 in interest. One tier is not trivial at the mortgage scale.

- Pushing from 750 to 780 saves only $24 per month and $8,596 in interest. The top of the scale is a narrow band. The expensive penalties are below 680.

This is the correction most credit articles get wrong. The savings curve is not a smooth slope. It is flat at the top and steep at the bottom. Reaching 750 captures the large majority of the available benefit.

Auto loan rates at a 750 credit score

Auto lenders tier by VantageScore, where 750 is Prime rather than Super Prime. Experian’s Q1 2026 data:

| VantageScore Tier | New Car APR | Used Car APR |

|---|---|---|

| Super prime (781 to 850) | 4.55% | 6.30% |

| Prime (661 to 780; 750 sits here) | 6.23% | 8.77% |

| Near prime (601 to 660) | 9.67% | 14.03% |

| Subprime (501 to 600) | 13.44% | 19.42% |

| Deep subprime (300 to 500) | 16.01% | 21.77% |

On a $30,000 new car loan over 60 months, the difference looks like this:

| Tier | Monthly Payment | Total Interest |

|---|---|---|

| Super prime | $560 | $3,598 |

| Prime (750) | $583 | $4,992 |

| Near prime | $633 | $7,953 |

| Subprime | $689 | $11,362 |

A 750 credit score saves about $2,961 against a near-prime borrower over five years. It costs about $1,394 more than a super prime borrower. Auto lending is the one product where the 750 to 781 gap has real money attached, because the Prime band is wide and 750 sits in its middle.

Credit cards with a 750 credit score

A 750 credit score clears the approval bar for essentially every mainstream rewards and travel card. Issuers reserve their strongest offers for this tier because the default risk is low and the spending profile is attractive.

What becomes available:

- Flagship travel cards with transferable points and airport lounge access

- Cash back cards with category rates commonly reaching 5%

- Introductory 0% APR offers on purchases and balance transfers

- Higher starting credit limits and faster limit increase approvals

- Better odds on credit limit reallocation and product changes

The APR you are quoted still depends on income and existing debt. A 750 credit score gets you the card. Your full financial profile sets the rate.

Renting, insurance, and utilities

Credit scores reach beyond lending.

- Landlords screen with credit reports and tenant screening scores. A 750 credit score generally clears the standard threshold without a co-signer or extra deposit.

- Insurers in most states use credit-based insurance scores to set auto and home premiums. These are separate from FICO or VantageScore, but they draw on the same report data, so the habits that produce a 750 usually produce a favorable insurance score.

- Utility and mobile carriers commonly waive security deposits for applicants in this range.

How a 750 Credit Score Is Calculated

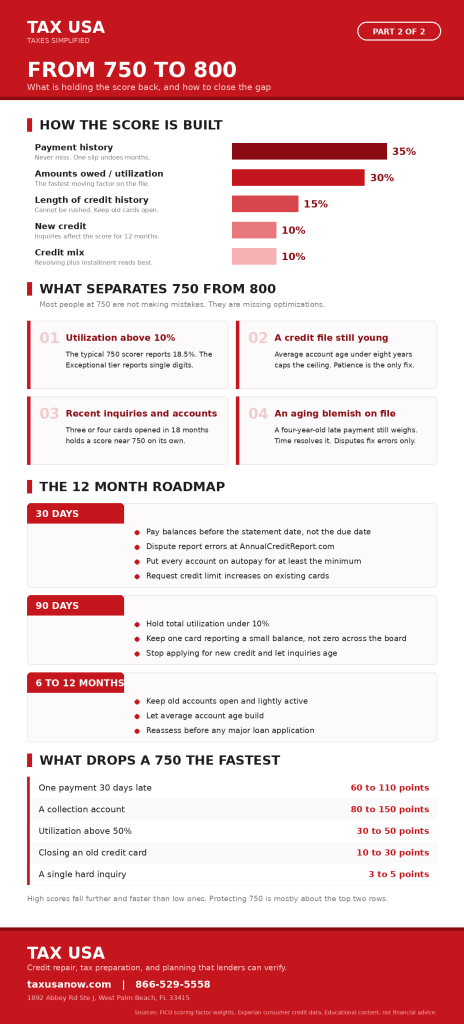

FICO builds the score from five weighted categories. Nothing else on your report matters as much as these five.

| Scoring Factor | Weight | What It Measures |

|---|---|---|

| Payment history | 35% | Whether you pay on time, and how badly you have missed |

| Amounts owed | 30% | Credit utilization and total balances |

| Length of credit history | 15% | Average and oldest account age |

| New credit | 10% | Recent hard inquiries and newly opened accounts |

| Credit mix | 10% | Revolving accounts alongside installment accounts |

Payment history at 35%

This is the single largest lever and the least forgiving one. A single payment reported 30 days late can cost a high scorer 60 to 110 points, and the higher your score, the further you fall. Late payments remain on the report for seven years, though their weight fades with time.

Amounts owed at 30%

Utilization is the fastest-moving factor on your report. It recalculates every statement cycle. The 750 average is 18.5%, which is exactly why so many 750 scorers stall there. Consumers in the Exceptional range typically report utilization in the single digits.

Length of credit history at 15%

Age cannot be manufactured. Your oldest account, your newest account, and the average age across all accounts all feed this factor. Closing an old card shortens the file and can raise utilization at the same time, which is why the advice to close unused cards is usually wrong.

New credit at 10%

Hard inquiries stay on the report for two years and affect the score for one. Rate shopping for a mortgage or auto loan inside a 45-day window counts as a single inquiry on newer FICO models, so comparing lenders does not compound the damage.

Credit mix at 10%

Lenders want evidence that you can manage both revolving and installment debt. A file with only credit cards caps out lower than a file with cards plus a mortgage or auto loan. This factor is small, and it is not worth taking on debt you do not need.

What Separates 750 From 800

Most people at 750 are not making mistakes. They are missing optimizations. The gap almost always comes from one of four places.

Utilization is sitting above 10%

At 18.5% average utilization, the typical 750 scorer is leaving points on the table. Reporting under 10% on the aggregate, with only one card carrying a small balance, is the profile that the Exceptional tier shares. Paying before the statement date rather than the due date is what controls the reported figure.

A credit file that is still young

An average account age below eight years limits the ceiling. There is no workaround for this beyond patience and keeping old accounts open and lightly active.

Recent inquiries and new accounts

Three or four cards opened in the last 18 months will hold a score near 750, even with perfect payment behavior. Both the inquiries and the lowered average age work against you at once.

An aging blemish still on file

A 30-day late from four years ago carries less weight than a fresh one, but it has not disappeared. Time resolves this. Nothing else legitimately does, unless the entry is inaccurate, in which case you have the right to dispute it under the Fair Credit Reporting Act.

How to Move From 750 to 800

Sequence matters here. Utilization changes fast. Everything else is slow.

Within 30 days

- Pull all three reports for free at AnnualCreditReport.com and dispute inaccuracies with the reporting bureau.

- Pay card balances down before the statement closing date, not the due date. The balance on the statement is what gets reported.

- Get every account onto autopay for at least the minimum. Payment history is 35%, and a single slip undoes months of progress.

- Ask for credit limit increases on existing cards. A higher limit lowers utilization without changing your spending.

Within 90 days

- Bring aggregate utilization under 10% and keep one card reporting a small balance rather than zero across the board.

- Add eligible utility, rent, and streaming payments through Experian Boost if your file is thin.

- Stop applying for new credit. Let recent inquiries age.

Within 6 to 12 months

- Keep old accounts open and put a small recurring charge on each so the issuer does not close them for inactivity.

- Let the average account age build.

- Reassess before any major application. If you are within a few points of a tier boundary, waiting a cycle can be worth thousands.

A realistic timeline from 750 to 800 is 12 to 24 months for most files, and it depends far more on account age than on effort. Any source promising 800 in 6 months is describing an unusual file, not a typical one.

What Can Drop a 750 Credit Score

| Event | Typical Impact | Recovery Time |

|---|---|---|

| Payment 30 days late | 60 to 110 points | 12 to 24 months to substantially recover |

| Utilization jumping above 50% | 30 to 50 points | 1 to 2 statement cycles once paid down |

| Closing an old credit card | 10 to 30 points | Permanent for age; immediate for utilization |

| Single hard inquiry | 3 to 5 points | 12 months |

| Collection account | 80 to 150 points | 7 years on report |

| Maxing out one card | 20 to 45 points | 1 statement cycle |

The pattern is clear. High scores fall further and faster than low ones. Protecting a 750 credit score is mostly about avoiding the top two rows.

Tools Worth Using

| Tool | What It Does | Cost |

|---|---|---|

| AnnualCreditReport.com | Official free reports from all three bureaus | Free |

| Experian Boost | Adds eligible utility, rent, and streaming payments to your Experian file | Free |

| myFICO Loan Savings Calculator | Shows rate and interest by score tier for mortgages and auto loans | Free |

| Issuer score dashboards | Monthly FICO or VantageScore tracking through your bank or card | Free |

| myFICO paid plans | Multi-bureau reports and multiple FICO score versions | Paid |

Free monitoring products typically show VantageScore 3.0, not the FICO version your lender pulls. Treat those numbers as a trend line, not a quote.

Where Tax USA Fits In

A credit score is one part of a financial picture that lenders read as a whole. Underwriters look at your score alongside your tax returns, your documented income, and your debt-to-income ratio. Self-employed borrowers and small business owners feel this most because an aggressive deduction strategy that lowers this year’s tax bill can also lower the qualifying income on next year’s mortgage application.

Tax USA works on both sides of that equation from West Palm Beach, Florida:

- Credit repair services for disputing inaccurate report entries and building a file that reads well to underwriters

- Individual tax preparation that documents income in a way lenders can verify

- Year-end tax planning that balances tax savings against loan qualification

- Real estate tax and advisory services for buyers and investors timing a purchase

- Bookkeeping and accounting services that keep the underlying records clean

If you are holding a 750 credit score and planning a mortgage, an auto purchase, or a refinance in the next year, the score is only one input. Contact Tax USA or call 866-529-5558 to review the full picture before you apply.

Frequently Asked Questions About a 750 Credit Score

Is a 750 credit score good or excellent?

A 750 credit score is Very Good on the FICO Score 8 scale, which runs 740 to 799 for that tier. VantageScore 4.0 calls it Prime. The CFPB classifies anything above 720 as superprime. It is not technically Exceptional, since that band starts at 800, but it qualifies you for near-best pricing on most products.

What mortgage rate can I get with a 750 credit score?

Based on May 2026 myFICO data, a 750 credit score falls in the 740 to 759 tier at an estimated 6.76% on a 30-year fixed mortgage at 80% LTV. That is 0.12 percentage points above the 780-plus tier. Your actual rate depends on your lender, LTV, DTI, loan type, and current market conditions.

How much does a 750 credit score save on a mortgage?

Against a 620 to 639 score, roughly $41,415 in total interest on a $300,000, 30-year loan. Against a 700 to 719 score, roughly $11,531. Against a 780-plus score, a 750 costs you about $8,596 more.

Can I get a car loan with a 750 credit score?

Yes. A 750 credit score sits in the Prime VantageScore tier, where the average new car APR was 6.23%, and the average used car APR was 8.77% in Q1 2026. The average new auto loan applicant scored 751, so a 750 is right at the market average for new vehicle financing.

How long does it take to go from 750 to 800?

For most files, 12 to 24 months. Utilization improvements can register within one or two statement cycles, but the remaining gap is usually driven by average account age and inquiry aging, and neither can be accelerated.

What is the fastest way to raise a 750 credit score?

Lower your reported credit utilization. It carries 30% of the score and updates every statement cycle. Paying balances down before the statement closing date and requesting credit limit increases are the two fastest legitimate levers available.

Can I rent an apartment with a 750 credit score?

Yes. A 750 credit score clears standard landlord screening thresholds in nearly every market. Income verification and rental history are typically the binding constraints at that score, not credit.

Will checking my own credit score lower it?

No. Checking your own score is a soft inquiry and has no effect. Only hard inquiries, generated when a lender pulls your credit after an application, can reduce your score, and those cost 3 to 5 points each.

Should I close credit cards I no longer use?

Usually not. Closing a card lowers your total available credit, which raises utilization, and it eventually shortens your average account age. Both work against a 750 credit score. Close a card only when an annual fee cannot be avoided by downgrading to a no-fee version.

Final Comments

A 750 credit score has already captured most of the financial benefit available on the FICO scale. The mortgage savings between 750 and 780 come to about $24 a month. The savings between 750 and 630 come to $115 a month and more than $41,000 over 30 years. You are on the flat part of the curve, and the priority shifts from climbing to protecting.

That means guarding payment history above everything, holding utilization under 10%, leaving old accounts open, and spacing out applications. Those four habits maintain the score. Time does the rest.

If a mortgage, refinance, or major purchase is on your calendar, review your score, your reports, and your documented income together rather than separately. Tax USA helps clients in West Palm Beach and across Florida do exactly that.